Savvy real estate investors can utilize a number of different tax-advantaged accounts to keep the most of their investment gains. The most popular are the 401(k) and the IRA, which allow investors tax deductions (or deferrals) for investing for their retirement.

Traditionally, most IRA providers only allow investors to invest in publicly traded and liquid securities, such as stocks, mutual funds, and bonds. Investors may want to invest in other options such as real estate, which has seen higher returns over the last 20 years than the S&P 500.

However, there are ways to invest in alternative assets with your retirement funds. Investors typically have the most cash available for investment and longest time horizon with their retirement accounts, making them perfect for investing in real estate.

Using Self-Directed IRA’s, investors are able to contribute their hard-earned retirement funds to buy investment properties, the same way they invest in stocks and bonds.

Arrived investors are able to use Checkbook IRA’s, a special type of self-directed IRA, to invest in rental homes directly on the Arrived platform. Arrived is partnered with Rocket Dollar, a self-directed IRA company that can help you create an account and invest your retirement funds.

What exactly is an IRA?

Here’s a very brief overview on the different IRA accounts. An Individual Retirement Account, or IRA, is a type of retirement account that anyone can open. The current contribution limits are typically $6,000 per year.

IRS rules give IRA’s advantages by being tax-advantaged. Contributions into the IRA can be pre-tax (Traditional IRA) or post-tax (Roth IRA). With both types, most companies only allow you to invest in stocks and bonds.

Investing with an IRA is a great way to take advantage of tax-deferred growth. The trade off is that since it’s a retirement plan, you have to wait until age 72 (or 70 ½ if you hit that age before January 1st, 2020) before you can begin to withdraw funds.

Once you hit that age, there are required minimum distributions (withdrawals) each year.

What’s a Self-Directed IRA and a Checkbook IRA?

A self-directed IRA is any IRA in which you’re able to invest in almost anything the investor wants. Most IRA companies don’t let investors do this because it’s extra administrative work for the trust company.

Investors who want more control over their investment options can choose to open a self-directed IRA. These accounts function the same as a regular IRA account, except the account owner has more options for how to direct their retirement funds.

There are two types of self-directed IRA’s. Most self-directed IRA’s are custodial accounts, meaning they require the custodian of the account to review the investment documents and ultimately sign on behalf of the IRA. These custodial IRA’s are not the kind of IRA that Arrived currently supports.

The other kind of self-directed IRA is a Checkbook IRA. With these accounts, the owner can sign investment documents on behalf of the IRA. Right now Arrived can only accept investments from Checkbook IRA’s.

A Checkbook IRA is a type of Self-Directed IRA (SDIRA) in which an investor can review and sign the paperwork themselves. These types of IRA’s have a slightly different structure than a regular IRA.

When you create a Checkbook IRA, investors first create a self-directed IRA account. Then investors create an LLC. The IRA custodian helps the IRA make 1 investment – into the LLC. The IRA account owner is the Manager of the LLC, and as such, can make investments on behalf of the LLC.

Voila! Now investors have an IRA that owns an LLC, and they have full control over how what that LLC makes investments into.

While this sounds complicated, it’s super easy to set up, and then it’s incredibly simple to start making investments. Arrived’s partnership with Rocket Dollar provides investors a one-stop shop for creating and managing your Checkbook IRA.

Why should I invest with a Checkbook IRA?

There are several great reasons to invest in real estate with a Checkbook IRA.

Money Ready to be Invested

For most investors, the bulk of their investible funds are in retirement accounts. You’ve already been working hard to save and invest for your retirement, and so Checkbook IRA’s are a great way to put your retirement dollars to work growing for you.

Smart investors utilize tax-advantaged accounts to grow their retirement nest-egg. For many investors, these retirement accounts are the largest source of investible funds.

With all that money saved over the years, it’s poised to be put to work by owning cash-flowing rental properties.

Time Horizon

Real estate works out the best as a long-term investment. This is because rents and home values have consistently appreciated over the long-term, even if there’s short term downturns in the housing market.

Real estate is also a great long term investment because it’s expensive to conduct real estate transactions. When you have a longer time hold period and time horizon, those costs are amortized over a longer period, which increases the overall returns.

Your retirement funds also have a long term focus! Investors already approach their retirement investing with a long-term focus, since IRA’s don’t let you withdraw without penalty until you turn 59 ½ years old.

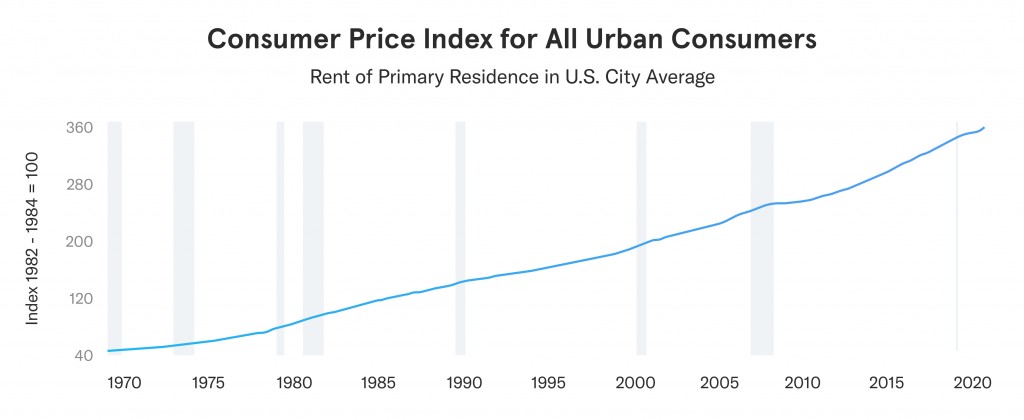

Over the long-term, rents have consistently appreciated over the last 50 years. This consistent growth is a big win for investors, particularly those who have a long time horizon, patience, and want their nest egg to be cared for.

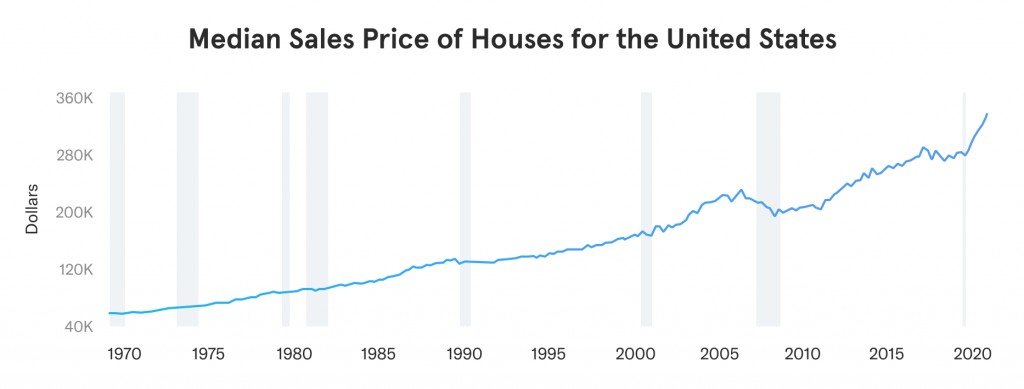

Prices for single-family homes have acted the same way. They’ve had larger booms and busts over the years, but over such a long time period they’ve consistently performed well when zooming out.

Even the dip in housing prices during the Great Recession looks tiny relative to 50 years of growth!

No Taxes on your Investments

With IRA’s, there are no taxes on the investment gains during the investment period. There’s no taxable income generated from the dividends, and when the property is sold there’s no capital gains for investors. Taxes are either assessed before making the contribution or when taking a distribution.

With a Traditional IRA, investors invest tax-free dollars but have to pay income taxes when they withdraw the gains.

With Roth IRA’s, investors invest already-taxed dollars into the account, and then they pay no income taxes when they withdraw funds in retirement.

For investors, this allows you to compound the investment returns. Instead of paying a portion of your gains each year to the IRS, you’re able to keep your money growing in the account, which helps for long-term growth.

Not paying taxes on your investment income each year allows your retirement funds to compound faster, creating more wealth for your family to access during your retirement.

One downside to investing your IRA funds in real estate is that you don’t get to benefit from depreciation. Normally depreciation reduces the taxable income, but all the income generated by your rental property won’t be taxed already since it’s within a retirement account.

Access to Alternative Investments

Investors no longer want to ride the roller coaster that is the stock market. There’s a rise in the popularity of alternative investment options as a means of diversification.

Alternative investments generally include investing in real estate, precious metals, or cryptocurrency. Basically, any investment strategy that isn’t easily available inside of a standard brokerage account.

Ryan Frazier, Arrived CEO, noted another reason that investors are becoming more interested in alternative investments:

“Guarding your portfolio against inflation and stock market fluctuations is another compelling reason to diversify with ownership of art, real estate and other investments. As the U.S. faces the most intense period of inflation in recent history, now might be a good time to take action.”

UBTI and UBIT Exemptions

Typically, IRA investments get penalized if they make investments that use debt (or leverage). They’re allowed to make those investments, but some of the income is considered taxable, which defeats the purpose of using the special tax-advantaged real estate accounts in general.

This is called Unrelated Business Taxable Income (UBTI), and then investors have to pay Unrelated Business Income Tax (UBIT).

The GREAT news for IRA investors is that Arrived investments are exempt from UBIT. Each Arrived property is taxed as a Real Estate Investment Trust (REIT), and as such they are excluded from any UBTI/UBIT scenarios, even though each property utilizes a non-recourse loan.

This is fantastic news for IRA investors! You’re able to invest into individual rental homes- that are each leveraged with 60-70% debt, and there are STILL no tax considerations!

Investing in Real Estate with a Self-Directed IRA

Investors who already have a Checkbook IRA have a number of different investment opportunities. Within the world of real estate, IRA owners can lend money or simply buy real estate. Investors can invest in residential, industrial, or commercial property.

To prevent the tax-advantaged benefits of a SDIRA from being abused, there’s lots of rules about what you can and cannot do. For example, an IRA owner can use debt to finance a property, but it must be a non-recourse loan.

There’s also a list of prohibited transactions, which are typically doing non-arm’s length deals with disqualified persons (like a spouse, sibling, or child). The IRS is wary of account owners trying to dodge taxes by making real estate purchases from family members.

IRA investors need to be very careful about the mechanics of investing with their IRA. By making transactions with family members or investments that use debt, they can accidentally cause a tax liability.

The great news is that with Arrived, both of these concerns are mitigated! As a 3rd party, investing with Arrived is not a prohibited transaction. And though the properties are mortgaged with a loan, the REIT structure of Arrived investments means there are no issues with the debt.

And of course, investors should always do their due diligence on any investment decision.

How to Get Started Investing with an IRA

To get started, you’ll first need to create a Checkbook IRA. Arrived doesn’t create these kinds of accounts, but our partner, Rocket Dollar, can help you get started.

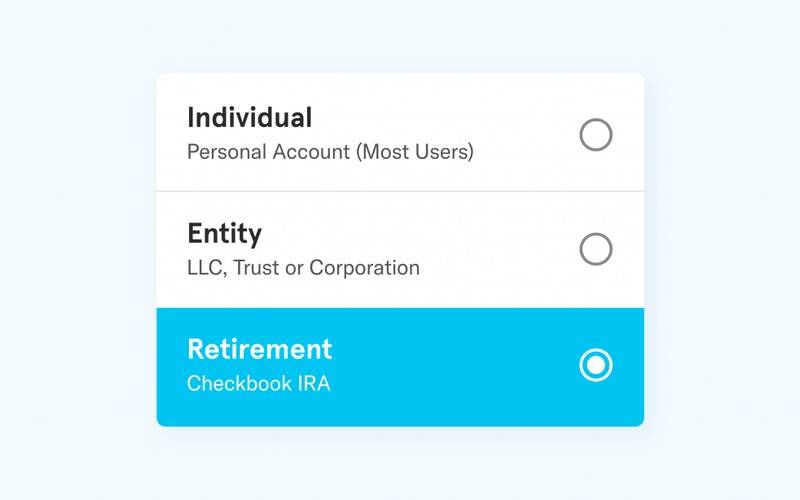

Once you have a Checkbook IRA account, you’ll be able to start investing with Arrived. Simply create a new Arrived account, and then in the account set up select “Retirement Account: Checkbook IRA”. By selecting this account type, you’ll be able to invest your retirement funds and Arrived won’t send you any tax forms.

Then you can start making investments! Your IRA will collect the rental income, which you can use to re-invest into new properties. Since your account is set up as a Retirement Account in our system, Arrived will not send you a 1099-DIV or any tax forms.

Watch your real estate holdings grow until you’re eventually ready to retire and enjoy the fruits of your investment.

Disclaimers: Arrived is not a financial planner or tax advisor, and you should consult with your advisors to make sure this is right for you.