In some cases, tax treatment can improve after-tax outcomes for real estate investments compared with fully taxable income sources such as high-yield savings accounts. But those outcomes depend on the structure of the investment, the type of income received, and each investor’s individual tax situation.

Here’s a closer look at how post-tax yield can help investors evaluate income-producing investments more clearly.

Why post-tax yields matter

The yields investors see advertised are typically shown before taxes. While those figures can be helpful for initial comparisons, they do not always reflect what an investor may actually keep.

The tax advantages of REITs

Some benefits that come from investing in REIT-qualified offerings include:

Passthrough income

REIT structures can avoid entity-level corporate income tax if applicable REIT requirements are met, potentially reducing the double taxation associated with traditional corporate structures.

199A QBI Deduction

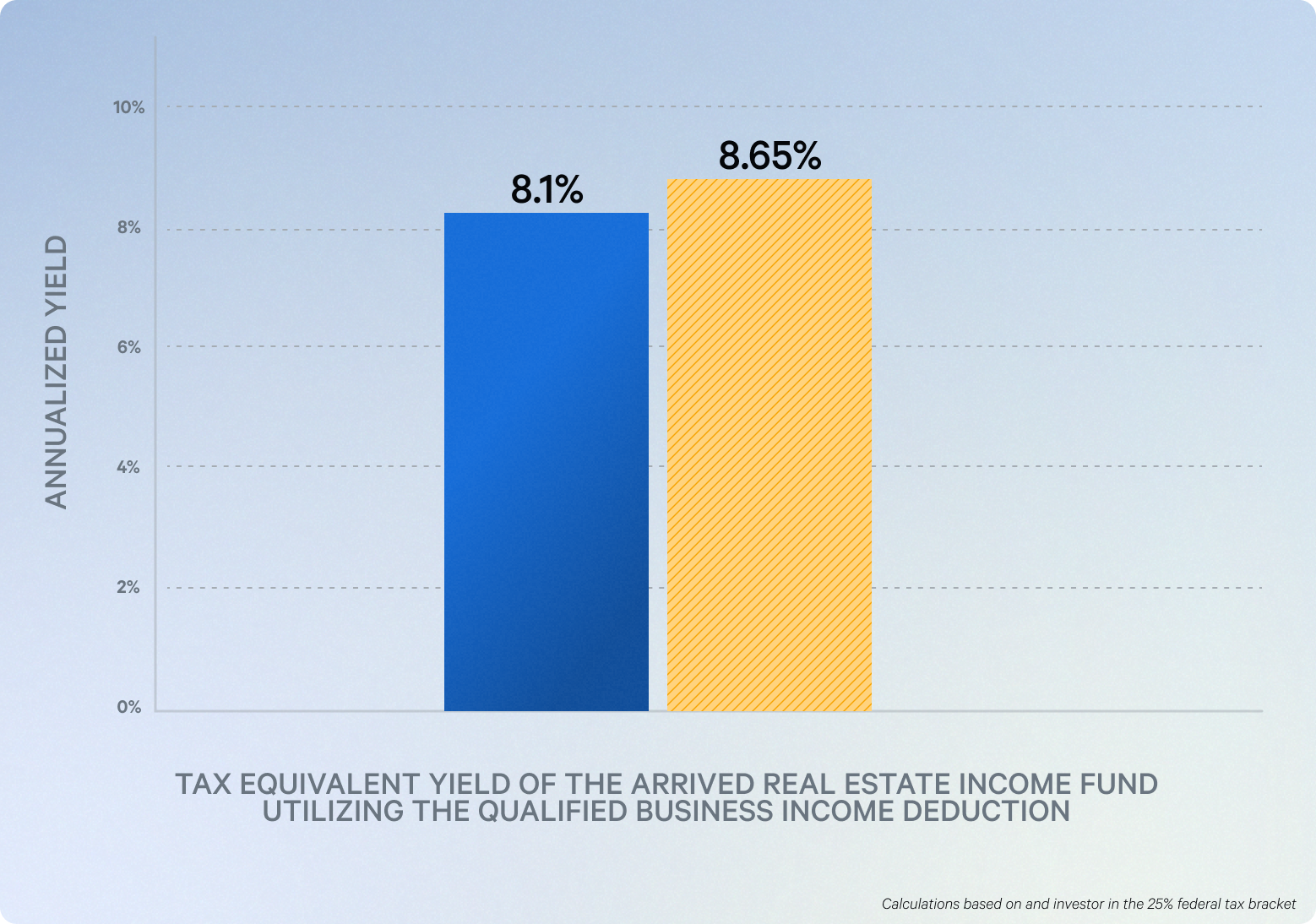

Certain qualified REIT dividends may qualify for the Section 199A deduction, which can allow eligible investors to deduct up to 20% of that qualified REIT dividend income, subject to applicable rules and limitations.

For example, an eligible investor in the 25% federal tax bracket could see an advertised yield of 8.1%¹ effectively increase to a tax-equivalent yield of approximately 8.65% when factoring in the Section 199A deduction.

Depreciation benefits for equity real estate investments

For equity real estate investments, depreciation can reduce taxable income even as properties generate cash flow. That tax deferral can improve after-tax outcomes over time.

It is important to distinguish this from real estate debt. Arrived’s Private Credit Fund is a mortgage REIT that invests in loans, so the tax treatment differs from equity real estate investments and does not rely on property-level depreciation in the same way.

Comparing post-tax yields to other investments

High-yield savings accounts

Fully taxable at ordinary income rates, these accounts yield far less after taxes. For an investor in the 25% federal tax bracket, a 4.75% yield becomes just 3.56% post-tax.

Private credit funds

Investments in Arrived’s Real Estate Income Fund with an 8.1%+ historical annualized yield¹ and the 199A deduction result in a post-tax yield of 6.48%. That’s nearly double the post-tax yield of a high-yield savings account, offering a compelling case for these tax-efficient investments.

Why timing matters

The Section 199A deduction remains available under current law

Certain qualified REIT dividends may still be eligible for the Section 199A deduction, which can allow eligible investors to deduct up to 20% of that income. The IRS continues to maintain current Section 199A guidance and filing forms, including Forms 8995 and 8995-A. Because tax treatment depends on the type of income received and each investor’s situation, investors should consult a qualified tax advisor about how current rules apply to them.

Tax considerations matter year-round

Taxes can have a meaningful impact on what investors ultimately keep from an investment. That is why post-tax yield can be a useful lens when comparing income-producing investments, not just during tax season, but throughout the year.

Market comparisons are favorable

When comparing income-producing investments, pre-tax yield does not always tell the full story. Traditional savings products are generally taxed at ordinary income rates, while certain real estate investments structured as REITs may benefit from different tax treatment, including potential Section 199A eligibility for qualified REIT dividends. Depending on an investor’s tax situation, that difference can affect after-tax outcomes.